Taking the first course in economics, being science students, when our professor asked us to graph the demand function (where demand is dependent on price), we all immediately plotted it with price on the x-axis and demand on the y-axis. That was my first lesson in marketing – the utilitarian concept; namely, quantity is always the primary variable. My lesson to always emphasize the consumer’s perspective, which being their need is the focal point of their decision-making process.

Later, as I started learning more, my second key lesson came from Edward Chamberlin’s theory of monopolistic competition. The idea that numerous firms sell differentiated products, allowing them some degree of market power or establishing a monopoly amongst their set of consumers. This differentiation is crucial in creating independent demand curves for each firm. For me, it was the crux of any marketing strategy from product differentiation to market segmentation to brand loyalty to customer lifetime value.

Implications for Consumer Home Lending

Why do I talk about these age-old theories now? I see two direct implications for consumer home lending (direct or indirect):

Understanding Borrower Needs and Market Challenges:

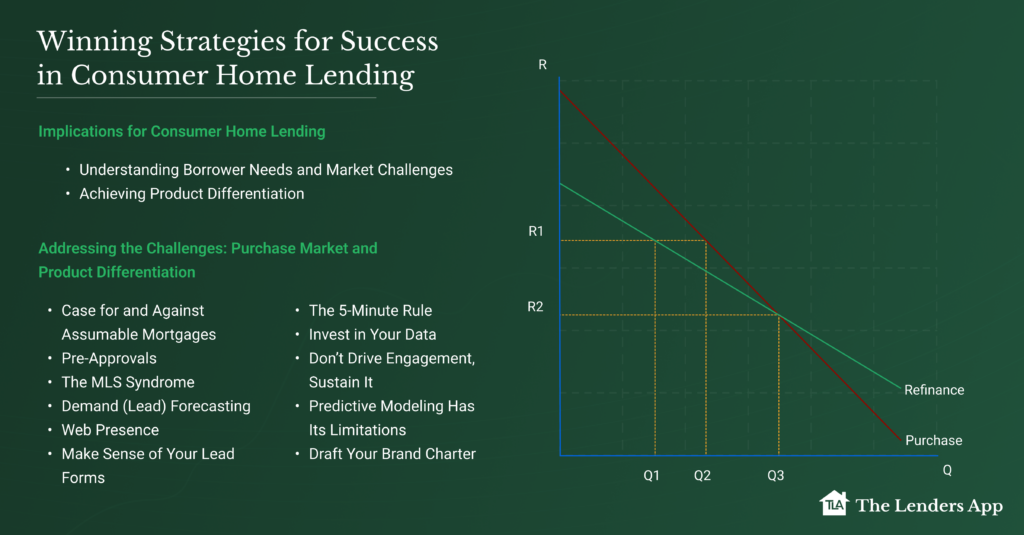

What is the borrower need that we are trying to solve for? And why is the purchase market so difficult for direct lenders? Logically, purchasing is more about homeownership and, therefore, taking a mortgage is an ancillary product like insurance. A borrower does not relate to the lender brand but to the realtor’s. Refinance, on the other hand, is more about money management and, therefore, relatively easier brand recognition for the lender. These are two separate needs and therefore two different curves.

Achieving Product Differentiation:

With interest rate being the key driver for mortgage choice, how do we attain product differentiation to comfortably identify with borrowers and ensure revenue returns? Technological advancements in processing have more or less normalized any incentives from higher pull-throughs or lower turn times. We have mastered the art of hyper-personalized direct marketing, exhausted and over-priced all relevant keyword approaches for SEM, targeted email lists to the point of maxed disengagement, provided as many talking points on a lead as possible to loan officers, drilled down on every cause/effect of satisfaction surveys, built referral networks around loan officers, created the most complex lead forms, tapped into digital servicing, explored all avenues of behavioral and credit leads, designed the most complex workflows on CRMs, and much more. Yet, other than prominent banks and one IMB, that magic touch eludes us.

And that one IMB needs a special mention. Rocket Mortgage has been methodical and scientific in their brand building. They recognize the need to operate on two separate demand curves, knowing that yield from one should counter yield from another in the long term – thereby settling into a hypothetical unified interest rate-originations plot which will be net positive from a CLTV perspective. They have been diligent about their brand architecture, and their long-term commitment has allowed them to find that key product differential.

Addressing the Challenges: Purchase Market and Product Differentiation

Here are some suggestions based on my experience:

1. Case for and Against Assumable Mortgages

The hype around assumption is not wrong. With a mortgage already tied to a property, this gives the lender a chance of putting the loan before the home. However, the market is small for assumable mortgages, and unless we see some NonQM products entering the space, it is likely to make little impact. But it’s something to think about.

2. Pre-Approvals

With interest rate being the key driver for mortgage choice, how do we attain product differentiation to comfortably identify with borrowers and ensure revenue returns? Technological advancements in processing have more or less normalized any incentives from higher pull-throughs or lower turn times. We have mastered the art of hyper-personalized direct marketing, exhausted and over-priced all relevant keyword approaches for SEM, targeted email lists to the point of maxed disengagement, provided as many talking points on a lead as possible to loan officers, drilled down on every cause/effect of satisfaction surveys, built referral networks around loan officers, created the most complex lead forms, tapped into digital servicing, explored all avenues of behavioral and credit leads, designed the most complex workflows on CRMs, and much more. Yet, other than prominent banks and one IMB, that magic touch eludes us.

And that one IMB needs a special mention. Rocket Mortgage has been methodical and scientific in their brand building. They recognize the need to operate on two separate demand curves, knowing that yield from one should counter yield from another in the long term – thereby settling into a hypothetical unified interest rate-originations plot which will be net positive from a CLTV perspective. They have been diligent about their brand architecture, and their long-term commitment has allowed them to find that key product differential.

3. The MLS Syndrome

We all run MLS trigger programs. According to NAR, 75% of the purchase market is for older constructions (not new), and about the same is for referral originations. We know only 30% constitute first-time buyers; the rest are buyers with prior mortgages. You do the math; whichever way you look, at least 50% of the purchase market would be for borrowers either moving or buying for investment/second homes. For long, our MLS programs have targeted borrowers, offering them new home purchase loans. Can we engage with them by helping them sell their current home? I think the whole MLS strategy needs to be re-examined.

4. Demand (Lead) Forecasting

Let’s be realistic. If the market is down, so will your forecast be. If your budgets are down, so will your lead volume be. Trying to maximize only results in bad leads, poor conversion, and wastage of time. Lead source analysis and optimization should be a priority, with each clearly showing what refinance and purchase volumes you would expect.

5. Web Presence

This is mandatory for product differentiation. A website is not meant only to capture leads but also to inform. A website is a data-driven strategic tool – content is not alone. And for folks who still are in doubt, a website is not expensive. It just requires nurturing. And therefore, yes, it is a very long-term investment.

6. Make Sense of Your Lead Forms

For the last 15 years, I have been modeling lead conversion rates based on lead data. I have used all tools and applied them to various forms. There is no silver bullet here. All I have concluded is that not all the information that you try to gather in a lead form is relevant. So why? I see lead forms for refinance, lead forms for conforming, lead forms for purchase, short-forms, long-forms, and many other versions on a single site. I don’t see a shopping cart for jeans, t-shirts, shorts, etc., when I shop at a garment retailer. It takes exactly 45 minutes to build a quick model and determine what is relevant and what is not on your lead forms. Try building one single, dynamic lead form. It will help you with Google indexing as well.

7. The 5-Minute Rule

I have heard enough about how contacting a lead within the first 5 minutes is critical. I disagree. I was running a credit trigger program back in 2018, and we saw that our conversions were highest on contacts between 23-30 days after the trigger date. I know why. It is lender specific, their processes, and the kind of customers that engage with them. No prospect, prospect lead source, and prospect’s reason to engage are the same. So why should the contact strategy be universal? Pay attention to what channel your customers like, the time of day, response patterns, response content, and use that to design your CRM workflows. I guarantee any CRM with basic features will work for you.

8. Invest in Your Data

I am not a critic of the reporting and data management capabilities of any CRM. They serve their purpose and do very well at it. But your data is yours; they cannot help you with it. We keep talking about modeling, machine learning, AI, and big data, but when it comes to saving our history and managing it, we resort to multiple Excel files with multiple tabs. Rarely opened, because they are mind-bending. Please believe that cloud computing is as secure as any on-premise servers. I think more secure, as they have multiple times the staff we have. Use it.

9. Don’t Drive Engagement, Sustain It

Haven’t you read enough about using digital technology to drive engagement? Engagement, at its very core, is a two-way street – two entities that come together and discuss a common purpose. If you think a digital strategy is going to “drive” engagement, forget it. Focus on long-term relationships built on interaction aided by digital channels. Sustaining relationships will benefit in overall customer value.

10. Predictive Modeling Has Its Limitations

There is no model that can confidently bucket prospects by propensity scores with pinpoint accuracy. Trust me, I have built and used many models, and the results have always been reasonable, not astounding. The reason is simple: each prospective borrower that initiates an engagement has a unique need. Unless they have sufficient time to waste filling out long, winding forms, it is often you who might not have a solution for them. My suggestion is to use predictive modeling for what it is meant for. Utilize modeling results to sharpen communication, optimize channels, and manage lead sources. Ensure these models are applied specifically to your data. Generic models will always yield generic results. Be clear about what your question is, what data you have, and have the insight to dig deeper into the modeling output.

11. Draft Your Brand Charter

It doesn’t matter if you are an individual broker or a large organization. You are not the brand that your business symbolizes. Write down its personality and then stick to it. Define what it stands for, what customers it wants to attract, and how it wants to grow; whatever comes to your mind. Then continue to stick to it, monitor it, and grow it. Mixing personalities, especially in indirect lending, often than not causes brand dilution.

In Conclusion

I have consciously tried to steer the conversation from “what sales and marketing should do” to “what we need to build as an organization” even before we start the “engagement” process. As a scholar myself, I don’t claim that these suggestions are all-encompassing. They are, however, a possible start. Setting ourselves up for success will have to be an inside-out process, irrespective of the tenets we follow.